Imagine opening your phone to check your bank balance, send money, split bills, invest, or even apply for a loan. All of this, but without stepping into a bank.

Sounds familiar, right? That’s because this is the new normal.

According to McKinsey, 73% of all banking interactions now happen digitally. That stat alone explains why FinTech is racing toward digital transformation.

In this blog, we’ll explore what digital transformation really means for FinTech, its impact areas, and real-world examples of how top banks and startups are driving change.

The Intersection Of Digital Transformation and FinTech

Consider you have the option to choose from the two apps:

A traditional FinTech app with basic features like bill payments, balance checks, and limited customer support.

A digital-first app with additional modern features like real-time transaction alerts, AI-personalized budgeting tools, integrated investing, crypto options, and 24/7 in-app support.

Which of the two would you choose? Of course, the second.

In this digital age, modern customers aren’t satisfied with just basic app functionalities. Instead, they want digitally transformed, customer-centric, and personalized experiences.

But here’s a thing: To provide the best digital experience, your business must integrate digital strategy in FinTech services as well.

Let’s explore key elements of digital transformation and their impact on the FinTech industry.

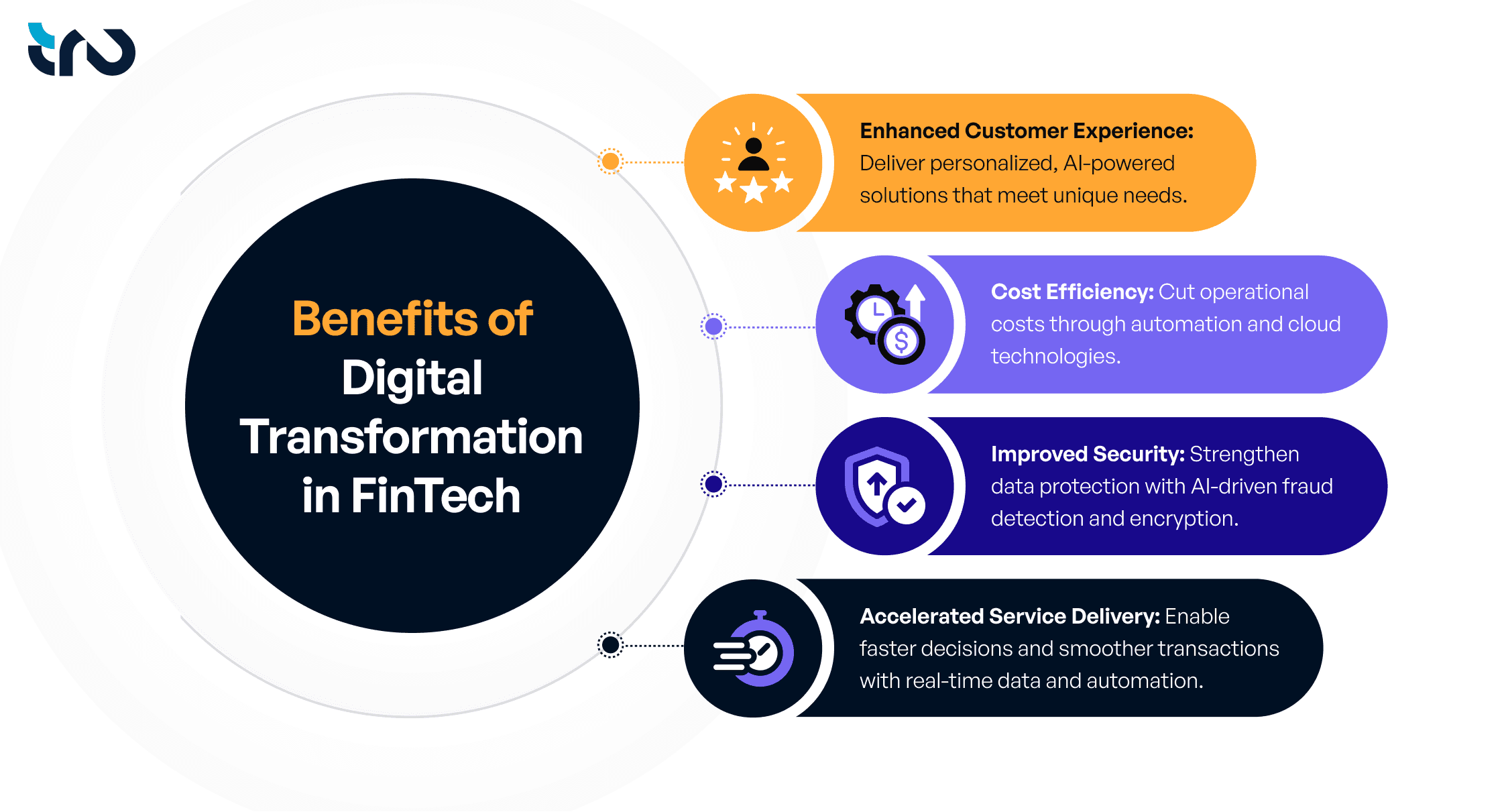

8 Key Elements of Digital Transformation in FinTech

Key Elements of Digital Transformation in FinTech

Element | Industry Trend | FinTech Digital Growth Impact | Tru’s Contribution |

|---|---|---|---|

Digital-First Strategy & Agile Delivery | Mobile-first adoption, agile product rollouts | Faster time-to-market, better user acquisition | Roadmap building, agile cloud setup, CI/CD pipelines |

Customer-Centric Experience | Rise of hyper-personalization expectations | Higher retention, deeper customer loyalty | UX/UI optimization, CDP/CRM integration, personalization engines |

Modern Infrastructure & Cloud Platforms | Accelerating Hybrid/Multi-Cloud Strategy | Scalable operations, global service delivery | Cloud migration, automated DevOps deployments |

Advanced Analytics & AI Integration | AI-driving smarter decisions in lending, fraud, and personalization | Predictive insights, faster risk evaluation | AI pipeline setup, ML model integration, real-time analytics dashboards |

Regulatory Tech & Risk Automation | Growing RegTech adoption for compliance efficiency | Lower compliance costs, faster onboarding | Automated KYC/AML systems, real-time risk engines, reporting workflows |

Process Automation & Operational Efficiency | Shift toward RPA and microservices architecture | Reduced operational costs, faster processes | RPA deployment, API-microservice orchestration, workflow automation |

Cybersecurity & Digital Trust | Security investment rising with digital adoption | Stronger brand trust, higher user confidence | DevSecOps practices, threat detection layers, infrastructure hardening |

Open Banking & Ecosystem Innovation | Surge in API-driven ecosystems, embedded finance | New revenue channels, broader platform reach | Open banking integrations, API management layers, ecosystem building |

1. Digital-First Strategy & Agile Delivery

Consumers are undergoing a rapid shift towards online-first experiences. A 2023 study by PYMNTS found that 47% of all new account openings in North America went to FinTechs and digital-only banks. So, FinTech businesses adopting mobile-first strategies and using data, AI are capturing a huge market share from legacy banks.

2. Customer-Centric Experience

With the rise of data analytics, personalization is no more an option but a need. Hence, top businesses like Revolut and Robinhood have already started offering customized spending analytics, real-time notifications, and targeted offers that keep users engaged and satisfied.

3. Modern Infrastructure & Cloud Platforms

FinTechs increasingly rely on scalable, cloud-native infrastructure to support growth and innovation. Thus, the majority of organizations have either adopted or are actively pursuing hybrid and multi-cloud strategies. This enables faster product launches and seamless global transaction processing.

4. Advanced Analytics & AI Integration

BCG finds that 49% of FinTech companies are “AI leaders” (the highest across industries). So, to compete and survive, FinTech businesses must implement AI/ML algorithms, credit scoring, fraud detection, and personalized financial advice. For instance, Kabbage (now part of American Express) uses AI models to quickly assess SME loan applications by analyzing data like transaction histories.

5. Regulatory Tech & Risk Automation

Compliance remains a cornerstone of FinTech operations. Hence, to meet evolving regulatory demands, it’s important to adopt automated risk engines and digital identity verification tools. Leading banks like Revolut and N26 use AI for real-time monitoring, while RegTechs like Plaid and ComplyAdvantage provide AML/KYC APIs to streamline compliance frameworks.

6. Process Automation & Operational Efficiency

To stay competitive, FinTechs are streamlining operations with automation and microservices. By adopting tools like robotic process automation (RPA) and API-driven workflows, they reduce manual tasks, cut costs, and speed up service delivery. This results in faster, leaner, and more scalable operations.

7. Cybersecurity & Digital Trust

According to Markets Media, finance, with 27% breaches, became one of the most breached industries in 2023. Thus, leading FinTechs like PayPal and Coinbase invest heavily in fraud engines and cold storage to build user trust. Also, security measures like MFA, end-to-end encryption, biometric logins, and continuous AI monitoring are no exception in today’s time.

8. Open Banking & Ecosystem Innovation

Open Banking adoption continues to accelerate, with over 58% of FinTech firms now offering API-based connectivity or “pay-by-bank” options (Source: Global Treasurer). This is unlocking new service models such as account aggregation and embedded finance. Platforms like Plaid and Yodlee provide underpinnings enabling secure data access and seamless transactions across ecosystems.

Ready to lead with a 360° digital transformation in FinTech? Explore Tru’s full suite of digital transformation services—from strategy and UX to data, AI, and cloud modernization—to future-proof your growth.

Real-World Examples: How Leading Banks Are Driving Digital Transformation

• Royal Bank of Canada (RBC)

RBC has invested heavily in cloud-native infrastructure and AI, migrating thousands of apps to a hybrid cloud. It launched solutions like “RBC Clear”, cloud cash management in under a year. Now in 2025, RBC partnered with Cohere to co-develop “North for Banking,” a secure generative AI platform.

• BMO (Bank of Montreal) Insurance

BMO Insurance introduced an Azure OpenAI–powered digital assistant for field underwriters in late 2024. This enables instant responses to complex product and policy questions, and improves speed and accuracy in life-insurance sales.

• Toronto Dominion (TD) Bank

TD has embedded AI in lending and insurance to accelerate decisions. In August 2023, TD introduced a machine-learning model (via its Layer 6 AI lab) that provides near-instant mortgage/HELOC pre-approvals for eligible customers.

• Canadian Imperial Bank of Commerce (CIBC)

CIBC has built its own generative-AI platform to boost employee productivity. In August 2024, CIBC announced CIBC AI, a proprietary large-language-model workspace for staff, alongside a rollout of GitHub Copilot for developers.

Conclusion

FinTech leaders today aren’t just adopting digital transformation—they’re building on it to stay competitive. From cloud to AI, these technologies are now essential to meeting customer expectations and reducing costs. The message is clear: adapt now, or risk being left behind.